No Events

Download all

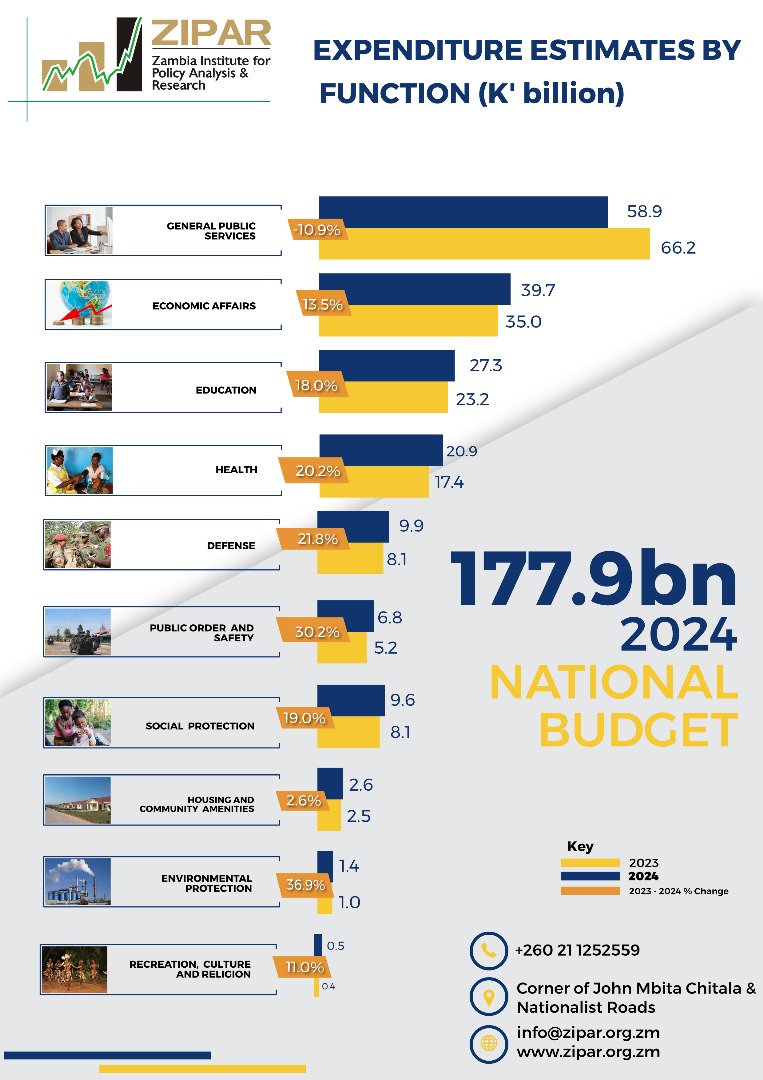

Budget Analysis

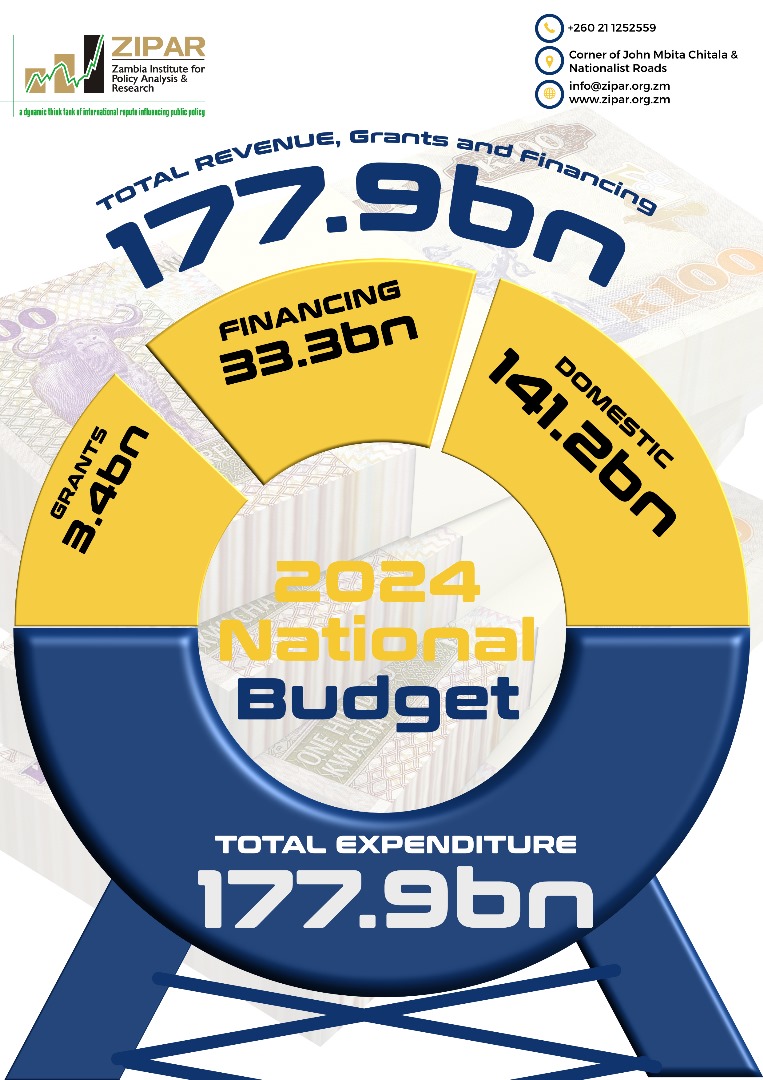

2024 Budget Analysis 2024 final web2

Size: 9.48 MB

Hits: 881

Date added: 27-11-2023

Date modified: 27-11-2023

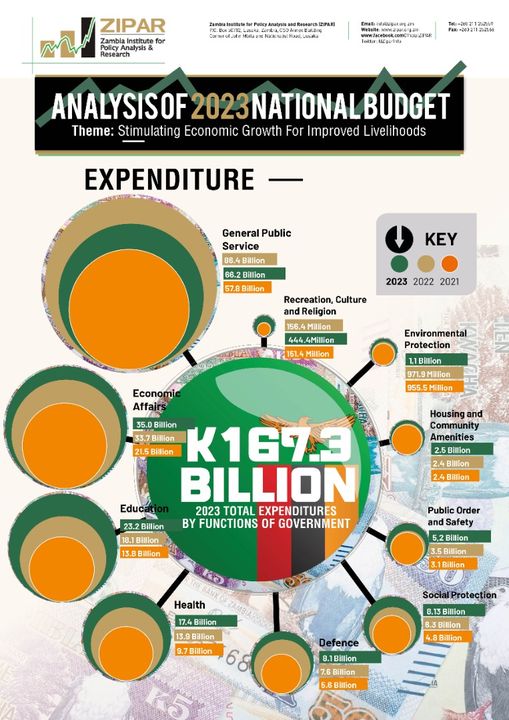

Analysis of the 2023 National Budget (2)

Size: 4.28 MB

Hits: 199

Date added: 27-11-2023

Date modified: 27-11-2023

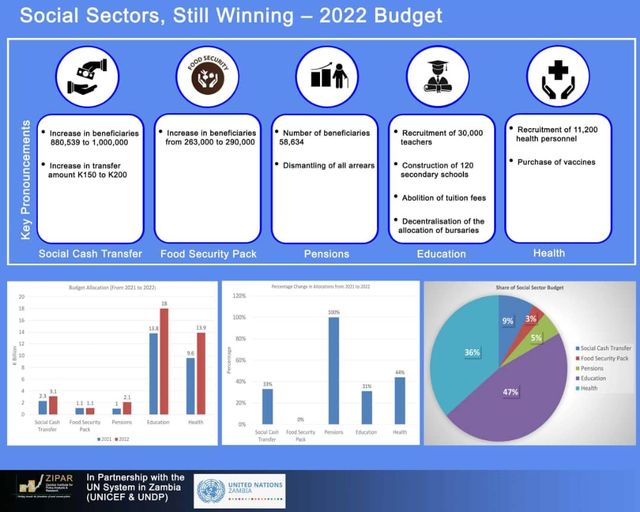

Analysis of 2022 National Budget (2)

Size: 952.26 KB

Hits: 163

Date added: 27-11-2023

Date modified: 27-11-2023

ZIPAR Review of 2021 Budget (2)

Size: 502.12 KB

Hits: 182

Date added: 27-11-2023

Date modified: 16-12-2023

Nurturing the seeds of Growth (1)

Size: 2.37 MB

Hits: 146

Date added: 27-11-2023

Date modified: 27-11-2023

TAKING THE ROAD LESS TRAVELLED 2019 Budget Analysis (1)

Size: 659.68 KB

Hits: 160

Date added: 27-11-2023

Date modified: 27-11-2023

Debt Servicing & the Delivery of Social Services (1)

Size: 504.58 KB

Hits: 156

Date added: 27-11-2023

Date modified: 27-11-2023

Download all

Strategic Plans

2018-2021 Strategic Plan_compressed

The development of the 2018-2021 Strategic Plan was necessitated by the expiry of the 2013-2017 Strategic Plan. The Plan was developed with technical support from Management Development Division (MDD), Cabinet Office. The process used integrated Institutional Assessment/Organisation Development/Balanced Scorecard (IA/OD-BSC) strategic planning approach.

Size: 1.40 MB

Hits: 172

Date added: 19-12-2023

Date modified: 19-12-2023